Spread analysis... 1

First, the influencing factors of intertemporal arbitrage... 2

Second, cracking price difference arbitrage influencing factors... 3

Third, cross-market arbitrage influencing factors... 6

Fourth, cracking spread arbitrage theory... 7

1. Cracking spread arbitrage classification... 7

2. Crude oil cracking spread arbitrage... 7

3. Case study with naphtha as an example... 8

4, case analysis: using 3:2:1 crack spreads to refine the oil profit... 9

V. Intertemporal price theory... 10

1. Overview of intertemporal price theory... 10

2. Take crude oil as an example for explanation... 10

3. Woking's theory of hedging theory... 12

Sixth, cross-regional spread theory... 13

1. Cross-market spread arbitrage brief description... 13

2. Cross-market spread arbitrage case analysis... 13

3, cross-market price arbitrage attention risk

Spread analysis

There are three main types of crude oil arbitrage, namely, cross-month arbitrage, cross-market arbitrage, and crack spread arbitrage. The different arbitrage factors are as follows:

I. Influencing factors of intertemporal arbitrage

Intertemporal arbitrage trading is a way of profiting from trading with fluctuations in spreads between different months of the same commodity. This method is one of the earliest and more mature arbitrage trading methods, and has become the first choice for investors seeking stable income.

To do a good job of inter-temporal arbitrage trading, we must first understand the fluctuations and returns of the price difference between the same commodity contracts. From the author's process of trading research, it mainly includes the following fluctuation factors:

1. Supply factors. Due to the progress of the production capacity of industrial products and the agricultural products of 000,061, the annual supply of different crops has led to changes in the near and long-term spreads. Such as the typical bull market premium and bear market premium.

2 , funding factors. The concentrated preference of funds for the target contract will cause fluctuations in the spread, such as shifting positions and squeezing positions.

3 , seasonal factors. Due to the seasonal characteristics of the production, trade and consumption of goods, the price difference between contracts is strong. For example, the annual output of agricultural products is sold; the seasonal purchase of non-ferrous metals; the difference in consumption of crude oil during the off-season;

4 , weather factors. As near-month contract prices are more sensitive to short-term weather changes, the near-far spreads fluctuate. For example, typhoon caused the interruption of crude oil production; bad weather affected short-term logistics and transportation.

5 , the rule factor. The rules governing the delivery of warehouse receipts will result in fluctuations in contract spreads at a certain point in time, such as contracts for the validity of warehouse receipts specified by rubber and plastics. In addition, the exchange adjustment rules will also cause fluctuations in the contract before and after the effective date. For example, this year's glass benchmark delivery adjustment resulted in significant differences in the 1505 and 1506 contract prices.

6. Policy factors. Due to the difference in the impact of policy adjustments on commodities in different periods, the spreads of different contracts fluctuated. For example, the adjustment of direct subsidies for soybeans and cotton has resulted in large fluctuations in the prices of new and old crops. In addition, changes in international trade policies will also lead to differences in price volatility in near-term monthly contracts. Such as trade protection, economic sanctions, etc.

7. Cost factors. The position cost has a fluctuation limit on the spread of the near-distance month contract, that is, the far-month price is significantly higher than the recent month price, which may cause the price difference to return. If the non-ferrous metal contract price fluctuations are easy to be limited by the position cost. Eight is the expected factor. Expectations of economic development and price trends will also cause price spreads to fluctuate. In addition, as the far-month contract faces more uncertainty than the near-month contract, the sharp fluctuations in the distant months have led to changes in the near-far spread. Nine is other factors. For example, the impact of unexpected events on the price of recent months is greater, and the habitual operation of investment institutions.

Second, we must master the main trading patterns of inter-temporal arbitrage.

1. Forward delivery mode. Focus on the opportunity of the far-month contract is significantly higher than the near-month contract. Profit opportunities = far and near spreads - position costs.

2. Spread trend mode. Once the trend is formed, it will not change easily, and the trend of the spread will be the same. This model focuses on homeopathic trading opportunities after the spread trend has been established.

3. Return to the trading mode. By analyzing the distribution of historical spreads and the law of operation, when the spread deviates from or approaches the boundary of the historical fluctuation zone, the spread arbitrage returns to the transaction.

4. Statistical arbitrage mode. The trading model uses high-speed and large-scale statistics to establish the strong and weak relationship of different contracts and open positions based on this. Generally only do intraday trading, that is, the arbitrage transaction ends before closing.

Second, cracking price difference arbitrage influencing factors

1 , seasonal impact

Gasoline accounts for 53% of crude oil products and 59% of total operating income, which is affected by gasoline prices in spring and summer.

US June driving season). Spring refining profit is the dominant factor in the year-round profit. In winter, gasoline prices have fallen and inventories have risen. Therefore, in general, refining profits in the second and third quarters are high and winter is low.

Distillate oil has seasonal demand and price trends opposite to gasoline. Although the rise in distillate oil in the autumn helps to adjust profits, it does not make up for the strong seasonal and summer demand for gasoline and the seasonal impact of the winter downturn. The main reason is that compared to gasoline, distillate oil has a small proportion of production (only 23% of Brent crude oil production, and 53% of gasoline).

2. The impact of refining capacity utilization capacity on cracking profit

In general, when the production capacity limit is approached, the marginal production cost rises (idle high-capacity capacity is used to meet more demand) and the production price rises.

Despite this, refining companies will not suddenly face the upper limit of production capacity, there is a certain flexibility to adjust the space (mixed use of lighter crude oil, reduce the capacity of downstream units, or buy other countries' refined oil). The importance of capacity constraints can only cause dramatic changes when the final critical increment is reached. The downstream capacity utilization rate has increased, and the elimination of bottlenecks has also brought about a certain improvement in variable costs.

At present, there is still no absolute quantitative way to prove the relationship between refining capacity utilization/cracking profit.

3. Refining capacity utilization rate

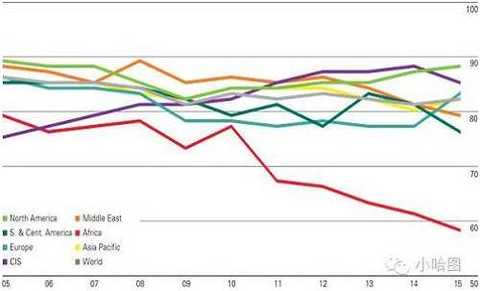

In addition to the African refinery producing areas, other major refinery regions around the world maintain high capacity utilization rates, reaching 80-90%.

|

Figure 1: Seasonal factors affect the crack spread

Data Source BP, Yongan Futures Research Institute

4. The impact of reformed gasoline (RFG) regulations on cracking profits

The US Clean Air Amendment Act (CAAA) has the greatest impact on the profitability of reformed gasoline. It is a standard established to reduce the specifications of reformed gasoline for sulfurized diesel fuel. Therefore, it has a greater impact on Bonny light crude oil, and Arab light crude oil has the least impact. WTI is in between. The main reason is that Bonny crude oil contains naphtha with relatively high levels of benzene and benzene when processing naphtha. Although benzene has a high octane number, it is also carcinogenic and the RFG specification limits its specific gravity in gasoline. In order to meet the RFG specifications, refineries that have historically only used Bonny Light or Brent Brent have had to invest in new processes, such as isomerization to remove benzene from naphtha or to separate some naphtha.

However, although the reforming gasoline regulations have led to an increase in refining costs, they have not had an impact on refining margins (still dominated by the heavy crude oil price differential).

Comparison of refining profit between the Gulf of Mexico and the East Coast

The main production mode of the US refining industry:

It is mainly based on two Gulf Coast refinery models and one East Coast refinery model.

The model of the Gulf Coast refinery has a more complex refinery structure, including fluid catalytic cracking, coking and hydrotreating. One refinery model is designed to handle light crude oil, and the second refinery model represents the majority of crude oil products that can be produced, including gasoline, because of the larger coking unit and the more extensive hydrotreating than the first Handle high sulfur crude oil. In contrast, the East Coast refinery only has a fluid catalytic cracking (FCC) unit, but has no coking capacity and is designed to handle only low-sulfur crude oil.

5 , regional differences in refineries

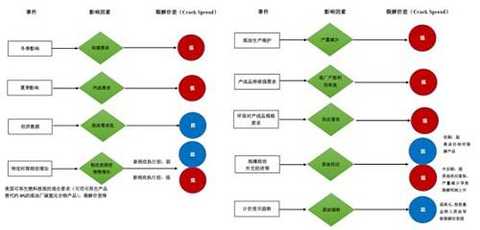

The Gulf of Mexico region has higher profits than the East Coast refinery. The Gulf Coast region has increased lighter/high value-added refinery output rates due to additional conversion facilities. The cost of the East Coast refinery does not reflect the advantages, resulting in higher profits in the Gulf of Mexico. Seasonal impacts result in smaller differences in profits between the Gulf of Mexico and the East Coast.

|

Figure 2: Summary of factors affecting the crack spread

Source: Yongan Futures Research Institute

Third, cross-market arbitrage influencing factors

Inter-city arbitrage is the act of arbitrage between two different exchanges. When the same futures product contract is traded on different exchanges, due to regional geographical differences, there will be different prices of such futures product contracts on different exchanges, that is, there is a certain price difference relationship, so traders can arbitrage through such phenomena.

We are more familiar with the arbitrage between the WTI crude oil of the New York Mercantile Exchange (NYMEX) and the London Intercontinental Exchange (ICE) Brent crude. For example, when the spread between WTI and BRENT crude oil futures is less than a reasonable level, the trader can buy the WTI crude oil contract and sell the BRENT crude oil contract. When the two market price differences return to normal, the contract will be hedged and profited. The opposite is true.

After the listing of INE crude oil futures, investors can pay more attention to the price difference between INE crude oil futures contract and WTI crude oil futures, the price difference between INE crude oil futures contract and BRENT crude oil futures, and grasp the cross-market arbitrage opportunities among them. Of course, futures arbitrage trading also has certain precautions. Inter-city arbitrage should pay attention to:

Transportation costs. Shipping costs are the main factor determining the spread of the same commodity variety between different exchanges. Generally speaking, the exchange price of the exchange close to the place of origin is lower, and the delivery is higher from the place of origin.

The difference in delivery grade. China's crude oil futures are medium-quality sulfur-containing crude oils. WTI and BRENT crude oil futures are light-weight sulfur-containing crude oils. Although cross-market arbitrage deals with the same variety, different exchanges have different regulations on the quality level of the products being traded. This also leads to price differences.

Trading units and exchange rate fluctuations. China's INE crude oil futures are quoted in RMB. WTI and BRENT crude oil futures are quoted in US dollars. When inter-city arbitrage, there may be problems with different trading units and quotation systems, which will affect the effect of arbitrage to a certain extent. If the market arbitrage in different countries, it may also bear the risk of exchange rate fluctuations.

Margin and commission costs. Inter-city arbitrage requires investors to pay margin and commission in both markets. Margin occupancy costs and commission fees are included in the cost of the investor. Only when the arbitrage spread between the two markets is greater than the above cost, investors can conduct cross-market arbitrage

Fourth, cracking spread arbitrage theory

The price difference between refined oil futures and crude oil futures in the same month. It is related to factors such as refined oil demand, refinery profit and operating rate. Cross-species arbitrage refers to the use of futures contract price differences between two different but interrelated commodities for arbitrage trading, that is, buying a futures contract for a certain commodity in a delivery month, and selling another same delivery month, Interrelated commodity futures contracts with a view to profiting both positions at the same time. Cross-species arbitrage must have the following conditions: First, the two commodities should be related and mutually substitute; second, the transaction is subject to the same factor; third, the futures contracts bought or sold should normally be in the same delivery month.

1, cracking spread arbitrage classification

Arbitrage between related commodities. There is a certain reasonable price difference between related commodities. When the actual price difference deviates from the reasonable price difference, there will be arbitrage space. That is, if the expected spread narrows, buy a low-priced contract and sell a high-priced contract.

Arbitrage between raw materials and finished products Under normal circumstances, there is a certain price difference between the commodities as raw materials and their processed products. When this price difference deviates from the normal range, the arbitrage between the raw material and the finished product can be performed. That is, if the expected spread narrows, buy a low-priced contract and sell a high-priced contract.

2. Crude oil cracking spread arbitrage

Crude oil cracking spread refers to the price difference between raw materials and products, that is, the price difference between crude oil and crude oil refined products. The crack spread is widely used in petroleum industry and futures trading, and can be expressed as the profit that the refinery expects to “crack†crude oil. space. Cracking spreads include gasoline cracking spreads, fuel oil cracking spreads, diesel cracking spreads, and naphtha cracking spreads. Among them, because naphtha belongs to the intermediate between crude oil and ethylene, the cracking price difference includes two aspects: the price difference of crude oil cracking to produce naphtha and the price difference of naphtha cracking to produce ethylene.

One of the factors that have the greatest impact on the crack spread is the relative proportion of the refinery producing various crude oil refining products. Of course, the demand for the refined oil and the start-up factors will also affect the crack spread. As long as there are gasoline, kerosene, diesel, Burning oil, aircraft fuel and asphalt. The crack spread is an indicator of a company's profitability. When the crack spread is higher, that is, when the price of gasoline or fuel oil rises relative to the price of crude oil, the profit of the refinery expands. When the crack spread is lower, the profit of the refinery decreases or loses. The expansion of the crack spread means that the profit margin of the product is higher, which means that there is a large room for the rise in the crude oil market. On the contrary, if the spread narrows, the profit margin is also lowered, and the product may have slow sales or excessive oil, then the crude oil in the market There is not much room for price increases.

3. Case analysis of naphtha as an example

Taking naphtha as an example: the ratio of raw materials to output is fixed during the refining cracking process. Under the incentive of expanding profits, the refinery will expand production capacity, thereby buying more oil and producing more naphtha. The increasing demand for crude oil has led to higher crude oil prices. The price of naphtha has decreased due to the increase in supply, and the final difference has decreased and profits have shrunk. The profit space of the refinery is reduced even to the extent of losses. The refinery will reduce production capacity, even stop production, reduce the purchase of crude oil, and even sell crude oil in stock, reduce the production of naphtha, and buy from the market. Naphtha will fulfill the previous sales contract so that the supply of crude oil in the market will increase, the price of crude oil will go down, and the supply of naphtha will decrease, and the price will eventually increase. I know that the profit of the refinery has risen again and the profit margin has reopened.

An oil refinery is located between the raw materials and finished goods markets. Crude oil prices and various refined oil prices are often affected by factors such as supply and demand, production conditions and weather of their respective products. Thus, the petroleum refinery is in a non-overall volatile market. There will be great risks in China. If the price of crude oil rises and the price of refined oil remains unchanged or even declines in a certain period of time, this situation will reduce the crack spread. The refinery realizes the purchase of crude oil and the sale of refined oil on the market. profit. Because refineries are at the same time in both aspects of the oil market, the risks they face in this market sometimes exceed those of retailers who sell crude oil alone or purchase refined oil separately. For a comprehensive oil company with production lines and sales lines, they have a natural economic hedge against market prices. However, for refineries that are only responsible for production, unfavorable market price trends will bring great economic risks. The profit of the plant is directly related to the price difference between crude oil and refined products, because the refinery can accurately predict all other expenses except the cost of buying crude oil, which is their biggest risk factor.

One way to control risk is to buy crude oil futures and sell finished goods futures. Simply put: most refineries use X:Y:Z cracking ratios to achieve hedging, where X, Y, and Z represent the number of barrels of liquid fuel from crude oil, gasoline, and fractions, respectively. The condition is X=Y+Z. In practice, the refinery will buy X barrels of crude oil in the futures market and sell Y barrels of gasoline and Z barrels of liquid fuel. In the actual situation, the crack spread is the price difference between trading crude oil, gasoline and distillate liquid fuel oil according to the ratio of X:Y:Z. The more widely used pyrolysis ratios are 3:2:1, 5:3:2, and 2:1:1. Since 3:2:1 is the most popular crack spread, the most widely traded crack spreads are GULF COAST3:2:1 and CHICAGO3:2:1. Another way is to buy a call option for crude oil and sell a put option for the finished product. Both strategies are complex, and the funds that are willing to hedge are also locked in the margin account. In order to reduce the transaction burden, many financial intermediaries in the commodity market have customized the product to facilitate the crack spread trade. For example, in 1994, the NYSE had a split price difference contract. NYMEX regarded the sale and purchase of multiple futures in this contract as a transaction. The contract was used to help the refinery lock in crude oil, oil and unleaded gasoline. The price establishes a fixed refinery margin. One of the spread contracts bundled three crude oil futures, two unleaded petrol futures and one hand-burning oil futures due after 1-2 months. This 3-2-1 ratio simulates the actual refinement of the three-way crude oil production of 2 barrels of unleaded gasoline and a barrel of fuel oil. Sellers and buyers of cracking contracts only need to consider the margin of this contract, without having to consider the respective margins of the various commodities involved in the contract. Therefore, refineries can lock in refining profits or arbitrage by simultaneously trading crude oil and refined oil contracts at a certain ratio, or by designing the holding positions of crude oil and refined oil to avoid the risk of cracking spreads.

The crack spread (theoretical refining yield) also uses the dollar/barrel unit of measure. To calculate this variable, the combined value of gasoline and diesel is first calculated and compared to the crude price. Because crude oil prices are expressed in US dollars per barrel and refined oil is expressed in cents per gallon, the price of heating oil and gasoline should be converted to USD/barrel in a ratio of 42 gallons per barrel. If the combined price is higher than the crude oil price, the overall refining yield will be positive. Conversely, if the common price is lower than the crude oil price, the cracking yield will be negative.

Using cracking spreads to hedge refining returns is a very good way to avoid risks. For example, if a refinery believes that crude oil prices will remain stable for a certain period of time in the future, or slightly increase, and refined oil prices may fall, the refinery can Selling the crack spread in the futures market means that the colleagues who buy the crude oil futures contract sell the gasoline and heating oil contracts. Once the refiner holds the short position of the crack spread, the refiner does not have to worry about the absolute price change of each contract. What he should care about is the relationship between the combined price of refined oil and the price of crude oil.

4, case analysis: the use of 3:2:1 crack spreads to refine the oil profit

In January, a refiner was considering his crude oil refining strategy and refined oil profits in the spring. He planned to set a two-month crude oil-distillate crack spread to hedge his refining gains. Monthly crude oil (18$/barrel) and May gasoline (53.21 cents/gal or $22.35/barrel) and May heating oil (49.25 cents/gal or $20.69/barrel) have a crack spread of $2.69/barrel. The ideal profit, so he sold the April/May crude oil-gasoline-heating oil crack spread in a ratio of 3:2:1, locked in the gain of $3.80/barrel, and bought the April crude oil contract to sell 5 Monthly gasoline contract and heating oil contract.

Since the futures market price reflects the spot price, the crude oil futures price is also $19/barrel, which he bought at $1/barrel, the price of gasoline rose to 54.29 cents/gal, and the price of heating oil rose to 49.50 cents/gal. The refiner closed the position on the futures market, buying gasoline and heating oil at 54.29 cents/gal and 49.50 cents/gallon respectively, selling crude oil at $19/barrel, and selling the entire crack. The yield on the spread position is 67 cents. If the refiner does not hedge, his income is limited to $3.13, and his income is actually 3.13 + 0.67 = $3.8, which is consistent with the profits he envisioned.

| time | Spot | futures | Spot income | Futures income |

| January | Sale crack spread Buying crude oil in April Selling heating oil for May Selling gasoline in May | $18 $20.69 $22.35 $3.8 | ||

| March | Buying crude oil for $19 Sell ​​heating oil for $20.79 Sold gasoline for $22.8 income | Buy crack spread Selling April crude oil Buying May heating oil Buying May gasoline income | 19 dollars, 20.79 dollars, 22.80 dollars, 3.13 dollars | 19 US dollars 20.79 US dollars 22.8 US dollars 3.13 US dollars 0.67 |

| No hedging gains | 3.13 dollars | |||

| Hedged income | 3.8 dollars | |||

V. Intertemporal price theory 1. Overview of intertemporal price theory

Inter-temporal arbitrage is a hedge against the same commodity but with abnormal changes in the normal price gap between different delivery months, and can be subdivided into two forms: bull market arbitrage and bear market arbitrage. Supply and demand are expected to change. Crude oil quarterly contracts are more active, and the distant month generally chooses quarterly months.

There are two types of monthly difference structures: Contango and Backwardation. When Contango expands to cover warehousing + capital costs, there is a risk-free arbitrage opportunity. The old cruise ship can be used to simmer oil (the storage fee is cheaper), and at the same time, the long-term futures are thrown, and the profit is locked. For example, in February 2016, the forward curve showed a depth of Contango, and the positive set was compressed to make the curve flat.

2. Take crude oil as an example for explanation:

1, positive sets and cases

In the WTI crude oil futures contract bull market arbitrage, buy the WTI crude oil futures contract in the recent delivery month, and also sell the WTI crude oil futures contract in the forward delivery month, hoping that the recent contract price increase is greater than the forward contract price increase; and the bear market Arbitrage, on the other hand, sells the recent delivery month contract, buys the forward delivery month contract, and expects the forward decline to be less than the recent decline.

For example of crude oil futures, please see the chart below:

| Bull market arbitrage (positive arbitrage) | Spread | ||

| July 1 | Buy 10 September WTI crude oil futures contract, price: 54 US dollars / barrel | Sold 10 November WTI crude oil futures contract, price: 59 US dollars / barrel | 2 USD / barrel |

| August 1 | Sold 10 September WTI crude oil futures contract at a price of $58/barrel | Buy 10 hands in November WTI crude oil futures contract price of 59 US dollars / barrel | 1 USD / barrel |

| Arbitrage result | Net profit of $4 barrel | Loss of $3/barrel | |

| Net profit = ($4 - $3) * 10000 barrel = $10,000 | |||

In the positive market, whether the spread is narrowed determines whether the arbitrage is successful. For crude oil futures, the monthly holding fee determines the spread between two adjacent delivery months. For two adjacent month contracts in the same crude oil production year, if the difference between the long-term month contract and the more recent month contract is greater than the position fee, it is expected that the future price difference will return to the position cost, then the colleague selling the long-term month will buy the recent month contract. It can be profitable, and the greater the spread, the smaller the risk and the greater the profit margin.

Interim arbitrage can be carried out on any crude oil futures variety, WTI and BRENT, as well as future crude oil futures contracts to be listed in China.

2. Reverse and case

If in the reverse market, the spread spread is beneficial to arbitrageurs. In addition, since the recent contract has no restrictions on the premium of the forward contract, and the premium of the forward contract to the recent contract is subject to the position fee, the profit potential of this bullish arbitrage is huge and the risk is limited.

| Bear market arbitrage (reverse arbitrage) | Spread | ||

| July 1 | Sold 10 September WTI crude oil futures contract, price: 54 US dollars / barrel | Buy 10 lots of November WTI crude oil futures contract, price: 54.5 US dollars / barrel | 0.5 USD / barrel |

| August 1 | Buy 10 September WTI crude oil futures contract, price 50 US dollars / barrel | Sell ​​10 lots of November WTI crude oil futures contract price 51 US dollars / barrel | 1 USD / barrel |

| Arbitrage result | Net profit of $4 barrel | Loss of $3/barrel | |

| Net profit = ($4 - $3.5) * 10000 barrel = $5,000 | |||

Contrary to the first example, whether the spread is expanded determines whether the arbitrage is successful. If the spread between the forward month and the recent month contract is less than the position fee, it is expected that the future spread will return to the position cost, then the competitor who buys the forward contract can profit from selling the recent contract. And the smaller the spread, the smaller the risk and the greater the profit margin. The positive market is subject to the position fee, while the recent contract in the reverse market can have a large premium for the forward contract, so this bear market arbitrage may have limited profit, and the possible losses are unlimited.

3. Woking's theory of hedging theory development

1. A brief description of Woking’s theory

Woking Theory: Woking Holbrooke is a well-known futures economist in the mid-20th century. He spent most of his life at Stanford University, and economic theory was mainly completed during Stanford University. The main achievements include: 1. Demand curve 2. Application of error theory to explain trend; 3. Differential price behavior in commodity price analysis; 4. Futures trading and hedging; 5. New concept about futures market and price.

This section mainly looks at Woking’s hedging theory.

The traditional hedging theory mainly comes from the theory of Keynes and Hicks. Based on the opposite position of the spot market and the futures market, the risk of the spot market is avoided. The traditional hedging theory follows the principle: the same type of goods, the goods The number is the same, the months are similar, and the trading direction is opposite. Due to the flaws in the traditional hedging theory, in 1962, Woking Holbrooke proposed the theory of hedging and hedging. He believed that hedging was not a speculation on prices, but a basis speculation. The core of hedging is not to eliminate risks, but to find profits by looking for changes in basis or expected basis for the New Year, that is, looking for opportunities through price changes in the futures market and the spot market. To avoid the small risk of changes in the spot market price, accepting the smaller risk of changes in the basis, Woking questioned the traditional hedging theory based on the idea of ​​risk minimization. He believes that hedgers are very similar to speculators because they They have positions in the spot market, so they are concerned with relative price changes, not absolute price changes. The essence of Woking Holbrooke's arbitrage theory is that hedging is seen as an arbitrage between spot and futures, profiting from two predictable price changes, rather than reducing risk. Therefore, hedging is seen as a basis for speculation, and it is a risk-free gain through high-selling and low-purchase basis.

In a perfectly competitive market environment, there are no transaction costs and taxes, etc. If the changes in the spot market price and the futures market price are consistent, then full hedging can be achieved, because one market profit can be used to make up for another market. Loss. However, in the real market environment, it is difficult to match the change in futures prices with the change in spot prices, and there is a risk of basis.

2. How to avoid the risk of basis:

Woking's hedging theory: the basis of the hedge is used to hedge the basis risk. The so-called basis-to-profit hedging means that the buyer and the seller negotiate to determine the magnitude of the agreement basis and determine the choice by the hedger. For the futures trading price, the traders in the spot market choose the commodity futures trading price of a certain day as the basis of valuation, and add the agreed price difference to the spot price of the two parties on the basis of the determined pricing. The price is delivered in stock rather than not considering the actual price of the commodity at the time of delivery.

The essence of the basis trade is that the hedger transfers the basis risk to the opponent of the spot transaction through the basis trade, and Woking proposes that the risk transferer will only carry out the hedging transaction if he believes that there is a profit opportunity. This kind of hedging behavior has the meaning of "speculation." In response to expected returns, Woking proposed two new concepts: 1. Selective hedging refers to hedging based on subjective judgments. When the conditions are favorable, only partial hedging is allowed and the part is left unprotected. 2. The expected hedging is that the operator holds a future contract in the futures market for a period of time and profits from the expected futures contract.

6. Cross-regional spread theory 1. Cross-market spread arbitrage

Inter-city arbitrage is the arbitrage trade between different exchanges. Due to the differences in geography and time and space, there is often a reasonable price difference between the same commodity in the futures markets of different countries. Usually, the spread will be stabilized in a fixed interval, and even if there is a short-term abnormality, it will eventually return to the normal level under the regulation of the market economy. This provides an opportunity for cross-market arbitrage across the globe.

Take the light sweet crude oil futures of the New York Mercantile Exchange (NYMEX) and the Brent crude oil futures of the London Intercontinental Exchange (ICE). When the spread between the two exceeds a reasonable level, investors can Buy the WTI crude oil futures contract and sell the Brent crude oil futures contract; after the expected spread narrows, you can hedge the trading contract (please pledge). In turn, buying a Brent crude oil futures contract and selling a WTI crude oil futures contract is a short-term arbitrage.

2. Cross-market spread arbitrage case analysis

Assume that on July 1st, NYMEX's December WTI crude oil futures contract price is $47/barrel, and ICE's December Brent crude oil futures contract is $50/barrel. The difference between the two is $3/barrel. If the arbitrageur believes that the spread will narrow (the opposite is true), there is arbitrage space, you can buy 10 WTI crude oil futures contract, sell 10 hand oil futures contract, and then wait for the opportunity to close the position at the same time profit.

| date | operating | operating | Spread |

| July 1 | Buy 10 December WTI crude oil futures contract at a price of $46/barrel | Sell ​​10 December Brent crude oil futures contract at a price of 51 yuan / barrel | 5 dollars / barrel |

| August 1 | The December contract price for selling 10 WTI crude oil futures is $47/barrel | Buy 10 December Brent crude oil futures contract at $50/barrel | 3 dollars / barrel |

| Arbitrage result | Earnings $1/barrel | Earnings $1/barrel | |

| Net profit = (1 USD / barrel + 1 / barrel) * 10000 barrel = $ 20,000 | |||

If the prices of the two contracts move in the same direction? If the Brent crude oil futures contract is less than WTI crude oil, then this trading strategy can still make a profit. According to the above assumptions, if the WTI crude oil futures contract also rises to $47/barrel on August 1, and the price of the oil-filled contract rises to $51.5/barrel, then the investor will still be able to make a profit of $5,000 after deducting the loss of $5,000.

| date | operating | operating | Spread |

| July 1 | Buy 10 December WTI crude oil futures contract at a price of $46/barrel | Sell ​​10 December Brent crude oil futures contract at a price of 51 yuan / barrel | 5 dollars / barrel |

| August 1 | The December contract price for selling 10 WTI crude oil futures is $47/barrel | Buy 10 December Brent crude oil futures contract at a price of $51.5 per barrel | USD 4.5/barrel |

| Arbitrage result | Earnings $1/barrel | Earnings $1/barrel | |

| Net profit = (1 US dollar / barrel - 0.5 US dollars / barrel) * 10,000 barrels = 5000 US dollars | |||

|

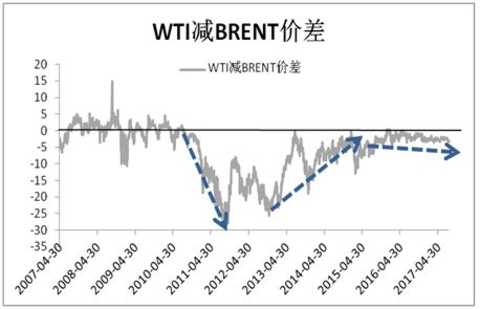

However, due to the construction of the oil pipeline and the lifting of the US export ban, the spread between WTI crude oil and Brent crude oil has been declining after experiencing the peak of 2015. Compared with the price difference of nearly $30, the price difference of $1-3 today is too small, which means that the arbitrage trading opportunities are less.

|

WTI-BRENT spread

Generally speaking, cross-market arbitrage must have the following three conditions: the quality of futures delivery targets are the same or similar; the futures varieties have strong correlations in the price movements of the two futures markets; the import and export policies are loose, and the commodities can be in two The country is free to flow. For example, in the previous period and the Dubai Commodity Exchange (DME), both futures contracts are marked with medium-quality sulfur crude oil and have a common customer base. They are two opportunities for perfect cross-market arbitrage.

If at the beginning of the listing, the domestic crude oil futures price is significantly higher than the Dubai crude oil futures price, it will lead to the delivery of a large amount of Middle East crude oil to the Chinese market. At that time, there will be an arbitrage opportunity to buy Dubai crude oil and sell domestic crude oil. On the contrary, if the domestic crude oil futures price is significantly lower At the Dubai crude oil futures price, then the demand for buying value will be stimulated, and then the arbitrage operation of buying domestic crude oil and selling Dubai crude oil can be implemented.

3, cross-market price arbitrage attention risk

The advantages of cross-market arbitrage are obvious. Since it is the difference spread of different contracts, the significant feature of the spread is that it usually has a lower volatility, and the risk of the factor arbitrage is also smaller. In addition, the spread is also easier to predict than the price. Arbitrage trading is not a direct forecast of price changes in future futures contracts, but a change in the spread caused by changes in future supply and demand relationships.

However, it should be noted that although cross-market arbitrage is a relatively stable method of maintaining value and investment, there are still certain risk factors. First of all, the spread relationship has relative stability only in a certain time and space. This stability is based on certain realistic conditions. Once such conditions are broken due to external factors such as tax rates, exchange rates, trade quotas, transportation costs, production levels, etc., or the price difference deviates from the mean, there is a lack of “regressionâ€.

In addition, when the market changes drastically, because the price fluctuations fluctuate too fast, some arbitrage with little space may have a price or a number of positions at any time during the opening or closing of the position, which leads to confusion of the entire arbitrage operation, directly affecting and Change the outcome of this arbitrage investment.

When unfavorable market changes occur in actual operation, remediation and position protection may be adopted for the method of adding, stopping or butterfly arbitrage of related varieties. When the loss exceeds the stop loss level, the stop loss strategy can be executed; when the loss does not reach the stop loss position, and the market is in the range oscillating state, the visualization is the upper and lower bottomed range fluctuations, and the cost is flattened by the jiacang. Ways to reduce losses; when the loss of one of the two varieties of cross-market arbitrage is too large, it can hold the varieties with greater correlation with the loss-type in the opposite direction of the investment ratio, thus hedging certain risks and preventingäºæŸçš„进一æ¥æ‰©å¤§ï¼Œæ¤æ—¶ä¾¿æž„æˆè¶å¼å¥—利。

(责任编辑:å´æ™“ç³HF106)

[Disclaimer] This article only represents the views of the cooperating contributors and does not represent the position of Hexun.com. Investors should act accordingly, at their own risk.

Printed T-shirts is our new fashions,this fabric is very soft and the main fabric is 95%cotton 5% spandex.daisy is printed in the left bust ,if u wear it,it will looks youth and full of sunshine,we have various kinds of colors for ur choice,by the way,if u have ur own design or other idea,u can also send us,we will according to ur requirements to do well.

Printed Shirts,Printed T-Shirts,Personalised T Shirts,Plain T Shirts For Printing

Shaoxing PinSheng Garment co,ltd , https://www.psfsshirt.com